Upsides and Downsides of Using Equity Release Mortgages Later in Life

Upsides and Downsides of Using Equity Release Mortgages Later in Life

Blog Article

The Crucial Aspects to Take Into Consideration Prior To Getting Equity Release Mortgages

Before getting equity Release home loans, individuals should carefully think about numerous essential aspects. Understanding the ramifications on their financial circumstance is crucial. This includes examining existing revenue, potential future expenses, and the effect on inheritance. In addition, discovering various product types and connected expenses is essential. As one browses these intricacies, it is necessary to evaluate emotional ties to residential or commercial property against useful monetary requirements. What other considerations might influence this substantial choice?

Comprehending Equity Release: What It Is and Exactly how It Works

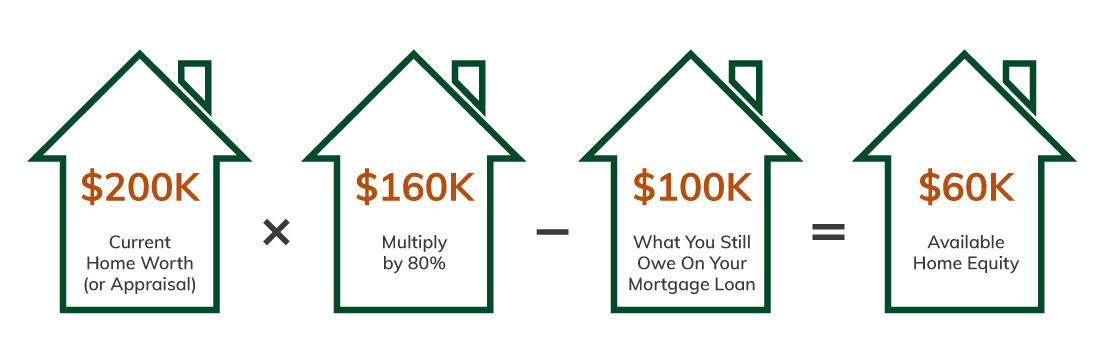

Equity Release enables home owners, usually those aged 55 and over, to access the riches locked up in their building without requiring to market it. This monetary option allows individuals to reveal a section of their home's worth, supplying money that can be used for various objectives, such as home renovations, financial debt payment, or improving retirement income. There are 2 primary sorts of equity Release products: lifetime home loans and home reversion plans. With a lifetime home mortgage, house owners preserve ownership while borrowing versus the property, paying back the funding and interest upon fatality or moving right into long-lasting treatment. On the other hand, home reversion involves selling a share of the property in exchange for a swelling sum, permitting the house owner to remain in the home till death. It is crucial for prospective candidates to understand the effects of equity Release, including the influence on inheritance and prospective charges related to the plans.

Assessing Your Financial Circumstance and Future Demands

Just how can a property owner successfully evaluate their financial circumstance and future requirements prior to taking into consideration equity Release? They should perform a complete assessment of their current income, expenses, and cost savings. This includes evaluating regular monthly expenses, existing financial obligations, and any type of prospective earnings resources, such as investments or pensions. Understanding capital can highlight whether equity Release is required for financial stability.Next, homeowners should consider their future needs. This involves preparing for possible health care expenses, lifestyle changes, and any kind of significant costs that may arise in retired life. Developing a clear budget plan can help in determining just how much equity might be needed.Additionally, talking to an economic consultant can provide insights right into the lasting effects of equity Release. They can help in straightening the home owner's financial scenario with their future goals, guaranteeing that any kind of decision made is informed and lined up with their overall economic well-being.

The Influence on Inheritance and Household Funds

The decision to make use of equity Release home mortgages can significantly influence household funds and inheritance planning. Individuals have to think about the implications of estate tax and just how equity distribution amongst heirs may transform as a result. These elements can affect not only the monetary heritage left but additionally the relationships among member of the family.

Estate Tax Implications

Although numerous house owners consider equity Release mortgages as a way to supplement retired life revenue, they may inadvertently impact inheritance tax obligation responsibilities, which can greatly affect household funds. When homeowners Release equity from their residential property, the quantity obtained plus interest builds up, reducing the value of the estate left to successors. If the estate exceeds the tax obligation threshold, this might result in a higher inheritance tax costs. In addition, any kind of staying equity may be deemed as part of the estate, making complex the monetary landscape for beneficiaries. Families have to realize that the decision to access equity can have lasting repercussions, potentially diminishing the inheritance planned for liked ones. Careful factor to consider of the ramifications is important prior to proceeding with equity Release.

Household Financial Planning

While taking into consideration equity Release home mortgages, households have to acknowledge the considerable impact these monetary decisions can have on inheritance and overall household finances. By accessing home equity, property owners may decrease the worth of their estate, possibly affecting the inheritance entrusted to beneficiaries. This can result in sensations of unpredictability or conflict among relative regarding future monetary assumptions. Furthermore, the expenses related to equity Release, such as interest prices and fees, can collect, decreasing the staying possessions offered for inheritance. It is crucial for family members to participate in open dialogues about these issues, ensuring that all participants comprehend the ramifications of equity Release on their long-term financial landscape. Thoughtful planning is important to stabilize prompt economic demands with future family heritages.

Equity Distribution Amongst Heirs

Equity circulation among heirs can substantially alter the monetary landscape of a household, especially when equity Release home loans are entailed. When a homeowner determines to Release equity, the funds drawn out might lessen the estate's general value, affecting what beneficiaries get. This reduction can lead to conflicts amongst household participants, specifically if assumptions regarding inheritance differ. Furthermore, the obligations connected to the equity Release, such as settlement terms and interest build-up, can complicate economic preparation for successors. Family members must consider how these variables influence their long-lasting monetary health and connections. Seminar concerning equity Release choices and their effects can help assure a clearer understanding of inheritance dynamics and reduce possible disputes amongst successors.

Checking Out Various Sorts Of Equity Release Products

When considering equity Release options, people can select from several distinct items, each tailored to different financial requirements and conditions. One of the most common kinds include life time mortgages and home reversion plans.Lifetime home loans permit home owners to borrow against their property worth while keeping ownership. The loan, in addition to accrued rate of interest, is repaid upon the home owner's death or when they relocate right into long-term care.In comparison, home reversion plans include selling a part of the home to a supplier in exchange for a round figure or normal repayments. The homeowner can proceed living in the residential property rent-free till death or relocation.Additionally, some products provide versatile features, enabling debtors to withdraw funds as required. Each product carries special advantages and considerations, making it necessary for people to evaluate their economic goals and long-term effects before choosing one of the most suitable equity Release alternative.

The Function of Rate Of Interest Prices and Costs

Picking the ideal equity Release product entails an understanding of numerous monetary variables, consisting of rate of interest and associated costs. Rates of interest can substantially affect the overall cost of the equity Release plan, as they identify how much the debtor will owe with time. Repaired prices offer predictability, while variable prices can vary, impacting long-term financial planning.Additionally, consumers must understand any kind of ahead of time charges, such as setup or appraisal fees, which can contribute to the first cost of the home mortgage. Ongoing costs, consisting of annual monitoring charges, can likewise collect over the term of the loan, possibly lowering the equity offered in the property.Understanding these prices is necessary for customers to assess the overall economic dedication and ensure the equity Release item aligns with their monetary objectives. Careful factor to consider of rate of interest and fees can help individuals make educated decisions that suit their circumstances.

Seeking Expert Suggestions: Why It is very important

Just how can individuals browse the complexities of equity Release home mortgages successfully? Seeking expert recommendations is a vital step in this procedure. Financial consultants and home mortgage brokers possess specialized knowledge that can brighten the details of equity Release products. They can supply tailored support based on a person's distinct financial scenario, ensuring educated decision-making. Specialists can assist clear up problems and terms, identify potential mistakes, and highlight the lasting ramifications of participating in an equity Release contract. In addition, they can aid in comparing various options, making certain that individuals select a plan that aligns with their needs and objectives.

Evaluating Alternatives to Equity Release Mortgages

When taking into consideration equity Release mortgages, individuals may find it advantageous Read Full Article to explore other financing alternatives that could better suit their demands. This consists of assessing the possibility of downsizing to gain access to funding while preserving financial security. A comprehensive analysis of these choices can result in even more educated decisions concerning one's economic future.

Various Other Funding Options

Downsizing Considerations

Downsizing provides a viable option for individuals thinking about equity Release home loans, especially for those seeking to access the value of their residential or commercial property without incurring added financial obligation. By marketing their present home and buying a smaller sized, much more economical property, homeowners can Release substantial equity while decreasing living expenditures. This option not just eases economic burdens however likewise simplifies upkeep duties connected with larger homes. In enhancement, scaling down might provide a chance to transfer to a preferred area or a neighborhood tailored to their lifestyle requires. Nevertheless, it is necessary for people to review the psychological facets of leaving a veteran house, along with the possible costs associated with relocating. Careful factor to consider of these aspects can lead to a more satisfying financial choice.

Frequently Asked Concerns

Can I Still Move Residence After Taking Out Equity Release?

The individual can still move home after securing equity Release, yet they have to ensure the brand-new residential or commercial property satisfies the lending institution's requirements (equity release mortgages). Furthermore, they may need to repay the funding upon moving

What Occurs if My Residential Or Commercial Property Worth Reduces?

The house owner may face reduced equity if a home's value lowers after taking out equity Release. Numerous plans use a no-negative-equity assurance, ensuring that settlement amounts do not exceed the building's value at sale.

Exist Age Restrictions for Equity Release Candidates?

Age limitations for equity Release applicants normally need individuals to be at least 55 or 60 years of ages, depending upon the supplier. These requirements assure that applicants are most likely to have sufficient equity in their property.

Will Equity Release Influence My Eligibility for State Perks?

Equity Release can potentially influence eligibility for state benefits, as the released funds may be thought about revenue or resources (equity release mortgages). People need to speak with financial advisors to understand how equity Release impacts their details advantage entitlements

Can I Pay Back the Equity Release Mortgage Early Without Penalties?

:max_bytes(150000):strip_icc()/dotdash-mortgage-heloc-differences-Final-6e9607c933e9467ba4d676601497a330.jpg)

Verdict

In recap, maneuvering with the complexities of equity Release mortgages calls for cautious factor to consider of numerous aspects, consisting of economic situations, future requirements, and the possible effect on inheritance. Understanding the different item options, linked costs, and the relevance of professional support is vital for making educated decisions. By visit this web-site thoroughly evaluating options and stabilizing emotional add-ons to one's home with useful financial needs, people can establish one of the most appropriate strategy to accessing their home equity properly (equity release mortgages). Developing a clear budget can aid in determining exactly how much equity might be needed.Additionally, seeking advice from with a monetary consultant can provide insights into the long-lasting implications of equity Release. Equity distribution among successors can greatly alter the economic landscape of a family members, particularly when equity Release mortgages are involved. Ongoing charges, consisting of annual administration charges, can also collect over the term of the car loan, potentially minimizing the equity readily available in the property.Understanding these prices is important for customers to examine the overall monetary commitment and guarantee the equity Release product straightens with their economic goals. If a building's worth decreases after taking out equity Release, the property owner may face decreased equity. Equity Release can possibly affect eligibility for state benefits, as the launched funds might be thought about earnings or capital

Report this page